App installieren

How to install the app on iOS

Follow along with the video below to see how to install our site as a web app on your home screen.

Anmerkung: This feature may not be available in some browsers.

Du verwendest einen veralteten Browser. Es ist möglich, dass diese oder andere Websites nicht korrekt angezeigt werden.

Du solltest ein Upgrade durchführen oder ein alternativer Browser verwenden.

Du solltest ein Upgrade durchführen oder ein alternativer Browser verwenden.

GT300 Spekulationsthread

- Ersteller p4z1f1st

- Erstellt am

Cordelier

Commodore Special

- Mitglied seit

- 04.03.2008

- Beiträge

- 390

- Renomée

- 66

Ja, wahrscheinlich. Allerdings nicht kaputt,sondern eher Ableger,Derivate. Z.B. GTX 465 ?Etwa auch all die kaputten Fermis?

Diese Zahlen meinen ja nicht Verkaufszahlen im Einzelhandel an Privat , sondern an Kartenhersteller u.ä..

Die 400.000 sind ja eine Abschätzung, "einige hunderttausend" - wird wohl mit >100K und <500K interpretiert. 200.000 wäre auch gut vorstellbar.

Aus dem vorläufigem SEC-Filing, ein ausführlicheres gibt es in ein paar Wochen, ergibt sich für ein Nvidia ein robustes Ergebnis. NV kann sich sehr gut behaupten, die Erwartungen des Marktes waren verständlicherweise aber höher. Die Zahlen für GPU und MCP(Chipsets) sind wie angekündigt zusammengelegt worden und zeigen sich oberflächlich betrachtet ähnlich dem Vorquartal.

Die Stückzahlen für diskrete GPUs stiegen ähnlich bei AMD leicht an, von 21,4 auf 21,9 Mio. gesamt.

Diskrete Desktop-GPUs-Zahlen fielen von 14,1 auf 12,7 Mio. ,wogegen diskrete Notebook-GPUs von 7,3 auf 9,2 Mio. zulegen konnten.

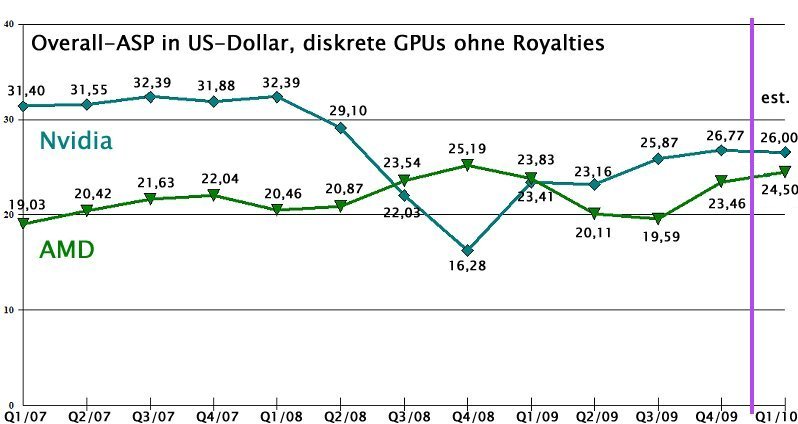

Da der GPU-Umsatz(ca. $573 Mio.) mutmaßlich ähnlich wie in Q4/09 war ergibt sich ein Overall-GPU-ASP von etwa $26,16, also leicht gefallen.Hier nochmal eine nicht mehr aktuelle Grafik(wg. Revidierungen) aus dem März.

AMDs ASP lag nach neuesten Berechnungen bei etwa $23,63 in Q1.

Interessanterweise gibt MR an das Nvidia in Q1 keine DX11-fähige GPU ausgeliefert haben soll. Vielleicht ein Mißverständnis oder man ist eben sehr korrekt.Bedeutet das im betreffendem Zeitraum vom 1.1.2010 bis 31.3.2010 keine Fermis verkauft wurden,Nvidias erste Quartal aber vom 1.2.2010 bis zum 2.5.2010 lief. Die besagten "einige hundertausend" müssten demnach insgesamt im April ausgeliefert worden sein.

Markus Everson

Grand Admiral Special

bbott schrieb:kann TSMC überhaupt soviel Wafer in 40nm herstellen bei der Yield (20- 30%)?!

Das frage ich mich natürlich auch. Allerdings stammt die Aussage über die Yield von vor dem Fermi Launch. Danach gabs eine Meldung von ... von wem eigentlich, TSMC oder NV?...das die Probleme mit der Yield nun gelöst seien.

Womit sich die Frage ergibt wie hoch der tägliche Ausstoß an 40nm Wafern für NV ist und wieviele davon (waren nicht schon vor ein paar Wochen 10 Mio 40nm GPUs von NV gemeldet worden?) Fermis sind.

Meine persönliche Spekulation: Die Gesamtzahl der 40nm GPU-Dice für NV beträgt mittlerweile einige Hunderttausend, nicht die der Fermis. Damit wäre die Aussage geeignet den Aktienkurs zum Nachteil der Aktienkäufer zu manipulieren was wiederum ein Straftatbestand wäre.

-> Der Kerl ist sowas von tot, selbst Michael Jackson ist gegen den Ganoven ein Springinsfeld.

Bevor ich hier was "beweisen" müsste, muss erst mal die Behauptung, die ich anzweifle, "bewiesen" sein, andernfalls brauch ich nix zu beweisen.

138 Mio $ Gewinn bzw. 13,8% Umsatzrendite sind knallharte Fakten für ein gutes Geschäft mit High-End Produkten. AMDs GPU Sparte hat nur eine Umsatzrendite von 11,4%, zudem hat AMD QQ Umsatz verloren währen NVIDIA QQ den Umsatz steigern konnte.

bbott

Grand Admiral Special

- Mitglied seit

- 11.11.2001

- Beiträge

- 4.363

- Renomée

- 60

- Mein Laptop

- HP Compaq 8510p

- Details zu meinem Desktop

- Prozessor

- AMD FX-8370

- Mainboard

- Asus M5A99X

- Kühlung

- Corsair H60

- Speicher

- 16GB DDR3-1866 Crucial

- Grafikprozessor

- Sapphire HD5770

- Display

- 4k 27" DELL

- SSD

- Samsung Evo 850

- HDD

- 2x Seagate 7200.12

- Optisches Laufwerk

- Pioneer, Plextor

- Soundkarte

- Creative X-Fi Xtreme Music

- Gehäuse

- Silverstone TJ-02S

- Netzteil

- Enermax 450W

- Betriebssystem

- Windows 7

Zeig mir doch mal einen Beweis für deine Behauptungen.

Könnte es einfach nur ein Missverständnis gewesen sein und nicht Hundert- sondern Zehntausend gemeint gewesen sein? Einfach eine Null zu viel? Was dann mit den bisherigen Gerüchten dann in etwa übereinstimmen würde.

Weil in der Größenordnung sollte doch eine bessere Lieferbarkeit fest zustellen sein, auch bei den Preise / Stromverbrauch und Lautstärke sollten die Nachfrage nicht all zu hoch ausfallen (siehe Geizhals.at).

Das alles in den Profikartenmarkt abgewandert ist kann ich mir kaum vorstellen, meist wird dort doch nicht das neueste vom neusten gekauft, da wird eher aus Ausgereift und stabile Produkte gesetzt. Es wird gewartet bis die Kinderkrankheiten beseitigt wurden.

Das ist zumindestens die Firmen Politik die ich kenne, Risiken und Arbeitsaufwand Minimierung.

Oder aber ein großer (Dell, Apple, HP,...) hat mal wieder in die vollen Gegriffen und alles aufgekauft

Die Meldung einfach Merkwürdig

Markus Everson

Grand Admiral Special

Werfen wir doch mal einen Blick auf das Transcript vom ConfCall

http://seekingalpha.com/article/205057-nvidia-q1-2011-earnings-call-transcript?page=6

Es ist tot, Jim.

http://seekingalpha.com/article/205057-nvidia-q1-2011-earnings-call-transcript?page=6

Ambrish Srivastava - BMO Capital Markets U.S.

Jen-Hsun, just to make sure that I understand your guidance. In the context of capacity and yield, should we assume that there are no constraints anymore and all the issues have been resolved?

Jen-Hsun Huang

I think the comment that David was making is that the yield has improved a lot. And TSMC has done a fabulous job, improving the yields of 40 nanometer since August of last year when we first ramped it to now. The yield and the number of wafers that they're able to produce, compound it, has really helped a lot. And so I think that with respect to manufacturability of 40 nanometers, I think we're surely out of the woods. I think we can now officially say that. We are clearly out of the woods, and I think that's all David was trying to say. The 40 nanometers at TSMC is now a world-class node and the manufacturability of it is very, very good. And so we're delighted with the execution from TSMC and they've just done a fabulous job. With respect to overall capacity, with respect to supply, the challenge is that the more and more customers are getting into 40 nanometers as well. And so we certainly aren't swimming in 40 nanometers supply. I mean we are constrained here and there. I wish we had more Fermis. I wish we had more GPUs of all kinds. And so there is still not enough 40 nanometers supply for the entire world, and so I expect that the 40 nanometer supply will remain constrained for sometime.

Es ist tot, Jim.

bbott

Grand Admiral Special

- Mitglied seit

- 11.11.2001

- Beiträge

- 4.363

- Renomée

- 60

- Mein Laptop

- HP Compaq 8510p

- Details zu meinem Desktop

- Prozessor

- AMD FX-8370

- Mainboard

- Asus M5A99X

- Kühlung

- Corsair H60

- Speicher

- 16GB DDR3-1866 Crucial

- Grafikprozessor

- Sapphire HD5770

- Display

- 4k 27" DELL

- SSD

- Samsung Evo 850

- HDD

- 2x Seagate 7200.12

- Optisches Laufwerk

- Pioneer, Plextor

- Soundkarte

- Creative X-Fi Xtreme Music

- Gehäuse

- Silverstone TJ-02S

- Netzteil

- Enermax 450W

- Betriebssystem

- Windows 7

138 Mio $ Gewinn bzw. 13,8% Umsatzrendite sind knallharte Fakten für ein gutes Geschäft mit High-End Produkten. AMDs GPU Sparte hat nur eine Umsatzrendite von 11,4%, zudem hat AMD QQ Umsatz verloren währen NVIDIA QQ den Umsatz steigern konnte.

Das liegt daran das viele nur NV kaufen, egal was es (mehr) kostet oder ATI bessere Produkte hat.

Als Grund werden dann z.B. die "schlechteren" Treiber angeführt. IMAGE ist alles.

Solange das so ist, wird ATI kaum eine bessere Umsatzrendite hin bekommen als nv, außer ATI voll bringt noch Wunder

.

EDIT :

.

@ Markus Everson

War nicht sogar teilweise ein Rückschritt auf 55nm in Planung?

[IRONIE] Aber wenn her Jen-Hsun Huang das sagt, dann ist nun in 40nm ja alles in Butter. [/IRONIE]

Will uns dann ATI keine 5800er verkaufen? Oder warum wird dann der Mark dann nicht mir 5800er überschwemmt? Die Lieferbarkeit ist immer noch alles andere als Optimal.

Als nächstes wird uns Jen-Hsun Huang mitteilen, dass beim GF100 die Ausbeute besser ist als beim RV870. Wir haben die Werte falsch Interpretiert die 20% waren nicht Ausbeute sondern Ausschuss

Dr@

Grand Admiral Special

- Mitglied seit

- 19.05.2009

- Beiträge

- 12.791

- Renomée

- 4.066

- Standort

- Baden-Württemberg

- Aktuelle Projekte

- Collatz Conjecture

- Meine Systeme

- Zacate E-350 APU

- BOINC-Statistiken

- Mein Laptop

- FSC Lifebook S2110, HP Pavilion dm3-1010eg

- Details zu meinem Laptop

- Prozessor

- Turion 64 MT37, Neo X2 L335, E-350

- Mainboard

- E35M1-I DELUXE

- Speicher

- 2x1 GiB DDR-333, 2x2 GiB DDR2-800, 2x2 GiB DDR3-1333

- Grafikprozessor

- RADEON XPRESS 200m, HD 3200, HD 4330, HD 6310

- Display

- 13,3", 13,3" , Dell UltraSharp U2311H

- HDD

- 100 GB, 320 GB, 120 GB +500 GB

- Optisches Laufwerk

- DVD-Brenner

- Betriebssystem

- WinXP SP3, Vista SP2, Win7 SP1 64-bit

- Webbrowser

- Firefox 13

Michael Hara schrieb:In the first quarter, we shipped a few hundred thousand units as yields have exceeded our expectations. The 480 and 470 are widely available worldwide and continue to sell out on a weekly basis. More importantly, being back in the Enthusiast segment is a positive driver of revenue and profitability growth.

David White schrieb:The core GPU business was flat quarter-over-quarter. Supply constraints are finally easing. In particular, yields of our high-end, Fermi-based GPUs were much higher than expected, leading to good availability of our new GeForce GTX 480 and 470 GPUs and Tesla high-performance computing products.

Quadro grew strongly once again and is now approaching pre-recession levels. Tesla had a record quarter, which together with our Quadro business, contributed to higher overall gross margin in the quarter.

Timothy Luke - Barclays Capital

If I may, could you guys elaborate on your comments associated with the increased availability of capacity, particularly on the high-end nodes? And also, your comment with respect to yields, on how you believe that may begin to impact your margin profile going forward?

David White

Yes, Tim. You'll recall that back in the fourth quarter and earlier times of last fiscal year, when we were ramping other products and the 40 nanometer node, we had many challenges with yields and our ability to supply the market with adequate product. And we really hit kind of a turning point, somewhere at around the December, January timeframe where we began seeing predictable improvements, and those improvements continued throughout the first quarter. And this being the first quarter that we launched Fermi, those wafer starts were done some time ago is a time when margins weren't as good as what they actually wound up being. And so our margin progression wound up exceeding our expectations. A result of exceeding expectations, we wound up having more die available to sell. Now given that Fermi only launched in the last three, four weeks of the quarter, there's only so much capacity you've got in the line when you exceed expectations like that. And we ship everything we can get to the back end, and that contributed to certainly, the quarter on margins. And going forward, we expect Fermi to continue to be an important element of our product mix. And as a result of that, you see our guidance of gross margin going up quarter-over-quarter as a result.

Timothy Luke - Barclays Capital

Your gross margin obviously going up with the revenue slightly down. The key catalyst for that is the Fermi ramp, is it? Or are there other elements that you might be able to elaborate on just on the strength of the gross margin in the coming quarter?

David White

Well, Fermi's a substantial piece of that. I mean our Tesla business is still continuing to grow, and so it'll become a bigger piece of the mix as well. But largely, it's Fermi and Fermi and Tesla, as well as Fermi and graphics.

...

Michael McConnell - Pacific Crest

Jen-Hsun, last conference call, you talked about Fermi and it would be hitting full stride in Q2 and that would offset seasonality, you guys have guided now seasonal. Has there been any change, regionally speaking, with demand? Any impact maybe Europe? Or any impact with memory pricing that has led you guys to back off a little bit and guide seasonal for Q2?

Jen-Hsun Huang

Well, we don't know anymore or any less about what's happening out in the larger market than anybody else. And there's, obviously, in the overall larger market, there are some concern about seasonality. But we are ramping Fermi as we had talked about before, and the success of Fermi is certainly as we expected. So when you see how it plays out here, I mean these are a couple of the -- with respect to Q2, those are the two dynamics that you're looking at. Seasonality on the one hand, on the other hand, we're ramping new products into a new segment that we've been out of for a couple of quarters, and so we'll see how it turns out.

...

Ambrish Srivastava - BMO Capital Markets U.S.

Jen-Hsun, just to make sure that I understand your guidance. In the context of capacity and yield, should we assume that there are no constraints anymore and all the issues have been resolved?

Jen-Hsun Huang

I think the comment that David was making is that the yield has improved a lot. And TSMC has done a fabulous job, improving the yields of 40 nanometer since August of last year when we first ramped it to now. The yield and the number of wafers that they're able to produce, compound it, has really helped a lot. And so I think that with respect to manufacturability of 40 nanometers, I think we're surely out of the woods. I think we can now officially say that. We are clearly out of the woods, and I think that's all David was trying to say. The 40 nanometers at TSMC is now a world-class node and the manufacturability of it is very, very good. And so we're delighted with the execution from TSMC and they've just done a fabulous job. With respect to overall capacity, with respect to supply, the challenge is that the more and more customers are getting into 40 nanometers as well. And so we certainly aren't swimming in 40 nanometers supply. I mean we are constrained here and there. I wish we had more Fermis. I wish we had more GPUs of all kinds. And so there is still not enough 40 nanometers supply for the entire world, and so I expect that the 40 nanometer supply will remain constrained for sometime.

...

Kevin Cassidy - Thomas Weisel Partners Equity Research

I wonder if you could give a little more detail on the inventory, the new product that didn't get packaged? Or if you could just give a little more details on that?

David White

Yes. Kevin, I think in the prior comments, and in the CFO commentary, we'd explained it really is associated primarily with GTX 470 and GTX 480. We ramped that product. We were favorably surprised with nicer yields than what we anticipated. And given the fact that our ramp was all occurring at the end of the quarter, there was just a limited amount of capacity we had at the back end to get everything out that we would've liked to have got now. And so when the quarter ended, we had some inventory of Fermi die that we need to package. [häääää??]

Shawn Webster - Macquarie Research

Just to close on the inventory, should we assume that channel inventory did increase globally? And Dave, in terms of the outlook for inventory, did you just say that you expect it to be flat? Or up? Or slightly down, or...

David White

No, I don't think I gave an indication other than the fact that we thought that inventory issues with Fermi at the end of the quarter would naturally work their way out as we fulfill demand in the channel and -- or other customers. [ich dachte man wäre "supply constrained"]

Jen-Hsun Huang

Shawn, the easiest way to think about the inventory situation is that we're ramping into Fermi, and we have a whole lot of ramping to do yet. The back-end cycle time, the amount of testing that we have to do for Fermi GPUs are longer than mainstream products because they're just much, much larger GPUs. The Fermi GPU, as you know, is some 3 billion transistors, and so there's a lot of testing to do in it. It takes longer to sort it. It takes longer to assemble it. It takes longer to test it. And then we do final system-level testing on the GPUs before we ship them. And so that entire back-end cycle time is many weeks. And so all of the dies that came out as we're ramping and you could imagine the curve on the ramp that we're ramping up right now, a lot of the die that came out of the fab we couldn't get through the back end before the end of the quarter, and so that's all part of inventory. Now of course we're ramping into a fresh new market and a fresh new product and there's a lot of pent-up demand, and so we just needed to keep the pressure on it and just keep cracking through it.

Shawn Webster - Macquarie Research

And how much as a percentage of your GPU revenues was 40 nanometer this last quarter?

Jen-Hsun Huang

Quite big, probably. Quite big.

David White

It grew quite nicely. And when you look at Fermi coming into the mix, along with our other 40-nanometer products, it grew pretty sizably this quarter.

Shawn Webster - Macquarie Research

And when you saw the yield upside, was that for across your whole range of 40 nanometer? Or was it pretty Fermi driven?

David White

It was across the whole 40-nanometer range.

...

James Schneider - Goldman Sachs Group Inc.

Could you address why accounts receivable jumped so meaningfully in the quarter?

David White

Well, we launched two products at the very end of the quarter, Fermi being one of them, right? And you launch those products at the end of the quarter, you end up with receivables that you collect on the next quarter. So its primarily all related to launch activities.

James Schneider - Goldman Sachs Group Inc.

So it's all the fact that the new products were still back-end loaded in the quarter?

David White

We launched them at the end of the quarter, and hence, they are back-end loaded again at the quarter, yes.

...

Glen Yeung - Citigroup Inc

As we think about the evolution of Fermi across the larger price stacking at NVIDIA over the course of the next few quarters, how should we think about that? What's the pattern we should expect to see? When does Fermi sort of permeate the entire price stack?

Jen-Hsun Huang

We are sampling Fermis from entry-level notebook all the way to supercomputer Fermis. So there are many versions that we're already sampling. So we're going to production with it as soon as our customers go into production.

Quelle: NVIDIA Q1 2011 Earnings Call Transcript

ansonsten ist alles "incredibly well", "ramping", "great", "big", "continue to grow"

Zahlen gibts aber keine:

Ambrish Srivastava - BMO Capital Markets U.S.

But there's no blended number that you would like to share with us?

Jen-Hsun Huang

I don't have anything to share with you right now.

BavarianRealist

Grand Admiral Special

- Mitglied seit

- 06.02.2010

- Beiträge

- 3.358

- Renomée

- 80

Es gäbe noch eine andere Interpretationsmöglichkeit für die "mehrere tausend Fermis":

An einer Stelle des Transcripts lese ich Folgendes:

"...

Jen-Hsun Huang:

We are sampling Fermis from entry-level notebook all the way to supercomputer Fermis. So there are many versions that we're already sampling. So we're going to production with it as soon as our customers go into production..."

So gesehen scheint Huang auch die kommenden ganz kleinen GF108 als "Fermis" zu bezeichnen, also all die kommenden DX11-Derivate von Nvidia. Und GF108 soll schon länger sein Tape-out hinter sich haben und könnte denmach auch schon in Produktion sein. Von diesen kleinen Dice schnell mal einige "hunderttausend" zu produzieren, dürfte nicht so das Problem sein.

Und schon wäre das "Problem" gelöst, oder

An einer Stelle des Transcripts lese ich Folgendes:

"...

Jen-Hsun Huang:

We are sampling Fermis from entry-level notebook all the way to supercomputer Fermis. So there are many versions that we're already sampling. So we're going to production with it as soon as our customers go into production..."

So gesehen scheint Huang auch die kommenden ganz kleinen GF108 als "Fermis" zu bezeichnen, also all die kommenden DX11-Derivate von Nvidia. Und GF108 soll schon länger sein Tape-out hinter sich haben und könnte denmach auch schon in Produktion sein. Von diesen kleinen Dice schnell mal einige "hunderttausend" zu produzieren, dürfte nicht so das Problem sein.

Und schon wäre das "Problem" gelöst, oder

So wie es schon einer sagte.138 Mio $ Gewinn bzw. 13,8% Umsatzrendite sind knallharte Fakten für ein gutes Geschäft mit High-End Produkten. AMDs GPU Sparte hat nur eine Umsatzrendite von 11,4%, zudem hat AMD QQ Umsatz verloren währen NVIDIA QQ den Umsatz steigern konnte.

Das Image von Nvidia ist noch sehr gut und ein gewisses Klientel rückt nicht so schnell ab.

Dazu war der Markt beschränkt, weil ATI nur 33% DX11-GPUs produzieren konnte und somit keinen großen Druck ausüben konnte.

Mit Fusion & North-Island kann sich eben vieles ändern.

Mit Fusion und Apple, könnte sich das Image von OpenCL deutlich verbessern (massentauglich), da Apple weiß, wie man Trends setzt bzw. das Image pflegt.

Mit North-Island @ GF sehe ich mehere Vorteile.

Einerseits die Kapazität mit GF.

Dazu vielleicht wie üblich sehr früher Einführung, wo dann AMD mit 28nm wieder länger einen deutlichen Vorsprung hat.

Andererseits das AF-Flimmern, welches sich schon mit der 5000er-Serie stärker verbessert hat. Die Blume ist ja schon schon Perfekt.

Ich denke, das AF-Flimmern hat relativ viel Wirkung.

Und wenn das so zutrifft, erst dann denke ich, könnte AMD an Nvidias Image kratzen.

PS: Ach ja, da gibts ja noch Physx & Optimus. Mal sehen, wie sich das entwickelt.

Nvidia hat halt verdammt viel gemacht, wo AMD eben aufholen muss. Aber sie sind auf einem guten Weg. Auch weil sie jetzt Konstanz zegien.

Wenn das stimmen sollte, dann sollte sich der Stromverbrauch auch verbessert haben. Und ein 512-Fermi sollte bald kommen.The 40 nanometers at TSMC is now a world-class node and the manufacturability of it is very, very good.

BavarianRealist

Grand Admiral Special

- Mitglied seit

- 06.02.2010

- Beiträge

- 3.358

- Renomée

- 80

"...The 40 nanometers at TSMC is now a world-class node and the manufacturability of it is very, very good..."

Danke für diesen Hinweis! Huang scheint es langsam zu übertreiben!

![:]](https://www.planet3dnow.de/vbulletin/images/smilies/rolleyes.gif "Augen rollen (sarkastisch) :]")

Soll ich bei der Aussage nun lachen oder weinen? Wer hält diese Aussage denn nicht für Unfug?

Wäre dem so, hätte TSMC längst in der Öffentlichkeit damit rum geprahlt. Digitimes wäre mit solchen News zu TSMC voll gewesen. Und AMD hätte längst keine Knappheit seiner GPUs mehr und bräuchte schon gar nicht auf alte 55nm-GPUs zurück greifen.

Danke für diesen Hinweis! Huang scheint es langsam zu übertreiben!

Soll ich bei der Aussage nun lachen oder weinen? Wer hält diese Aussage denn nicht für Unfug?

Wäre dem so, hätte TSMC längst in der Öffentlichkeit damit rum geprahlt. Digitimes wäre mit solchen News zu TSMC voll gewesen. Und AMD hätte längst keine Knappheit seiner GPUs mehr und bräuchte schon gar nicht auf alte 55nm-GPUs zurück greifen.

"...The 40 nanometers at TSMC is now a world-class node and the manufacturability of it is very, very good..."

Danke für diesen Hinweis! Huang scheint es langsam zu übertreiben!

Soll ich bei der Aussage nun lachen oder weinen? Wer hält diese Aussage denn nicht für Unfug?

Wäre dem so, hätte TSMC längst in der Öffentlichkeit damit rum geprahlt. Digitimes wäre mit solchen News zu TSMC voll gewesen. Und AMD hätte längst keine Knappheit seiner GPUs mehr und bräuchte schon gar nicht auf alte 55nm-GPUs zurück greifen.

Wenn 40nm bei TSMC nicht World Class ist, wieso lässt AMD dann dort den Llano fertigen?

Dr@

Grand Admiral Special

- Mitglied seit

- 19.05.2009

- Beiträge

- 12.791

- Renomée

- 4.066

- Standort

- Baden-Württemberg

- Aktuelle Projekte

- Collatz Conjecture

- Meine Systeme

- Zacate E-350 APU

- BOINC-Statistiken

- Mein Laptop

- FSC Lifebook S2110, HP Pavilion dm3-1010eg

- Details zu meinem Laptop

- Prozessor

- Turion 64 MT37, Neo X2 L335, E-350

- Mainboard

- E35M1-I DELUXE

- Speicher

- 2x1 GiB DDR-333, 2x2 GiB DDR2-800, 2x2 GiB DDR3-1333

- Grafikprozessor

- RADEON XPRESS 200m, HD 3200, HD 4330, HD 6310

- Display

- 13,3", 13,3" , Dell UltraSharp U2311H

- HDD

- 100 GB, 320 GB, 120 GB +500 GB

- Optisches Laufwerk

- DVD-Brenner

- Betriebssystem

- WinXP SP3, Vista SP2, Win7 SP1 64-bit

- Webbrowser

- Firefox 13

Wenn 40nm bei TSMC nicht World Class ist, wieso lässt AMD dann dort den Llano fertigen?

Was soll der Quatsch?

BavarianRealist

Grand Admiral Special

- Mitglied seit

- 06.02.2010

- Beiträge

- 3.358

- Renomée

- 80

Wenn 40nm bei TSMC nicht World Class ist, wieso lässt AMD dann dort den Llano fertigen?

Du meinst Ontario. Aber Ontario ist sehr klein vom Die her, dass sich das Yield da nicht so auswirkt. Da wird es halt dann haufenweise Single-Core-Ontarios geben

")

Wenn TSMCs Prozess "world-class" wäre, frage ich mich wirklich, wo denn Nvidias Fermis mit 512 funktionierenden Cores bleiben, vor allem nachdem sie ja angeblich schon "mehrere tausend" davon haben.

Leute, von Huangs Ausagen passt einfach nix, gar nix wirklich zusammen

Duplex

Admiral Special

Wenn 40nm bei TSMC nicht World Class ist, wieso lässt AMD dann dort den Llano fertigen?

Liano wird in 32nm SOI mit High K bei Globalfoundries gefertigt

Dr@

Grand Admiral Special

- Mitglied seit

- 19.05.2009

- Beiträge

- 12.791

- Renomée

- 4.066

- Standort

- Baden-Württemberg

- Aktuelle Projekte

- Collatz Conjecture

- Meine Systeme

- Zacate E-350 APU

- BOINC-Statistiken

- Mein Laptop

- FSC Lifebook S2110, HP Pavilion dm3-1010eg

- Details zu meinem Laptop

- Prozessor

- Turion 64 MT37, Neo X2 L335, E-350

- Mainboard

- E35M1-I DELUXE

- Speicher

- 2x1 GiB DDR-333, 2x2 GiB DDR2-800, 2x2 GiB DDR3-1333

- Grafikprozessor

- RADEON XPRESS 200m, HD 3200, HD 4330, HD 6310

- Display

- 13,3", 13,3" , Dell UltraSharp U2311H

- HDD

- 100 GB, 320 GB, 120 GB +500 GB

- Optisches Laufwerk

- DVD-Brenner

- Betriebssystem

- WinXP SP3, Vista SP2, Win7 SP1 64-bit

- Webbrowser

- Firefox 13

Liano wird in 32nm SOI mit High K bei Globalfoundries gefertigt

IMMER NOCH MIT ZWEI LLLLLLL

BavarianRealist

Grand Admiral Special

- Mitglied seit

- 06.02.2010

- Beiträge

- 3.358

- Renomée

- 80

Das Spiel von AMD mit Onatrio bei TSMC könnte auch so funktionieren:

Bekäme GF auch nix gebacken, braucht AMD weiter GPUs in 40nm bei TSMC und dann wohl auch erst mal erste Ontarios von TSMC, weil ja bei GF dann nix ginge.

Klappts aber bei GF, dann:

Wird AMD GPUs aus der GF-Produktion liefern, die Nvidia alt aussehen lassen. AMD wird möglichst viele GPUs bei GF fertigen, so dass Nvidia bald seinen 40nm-Kruscht nimmer los bekommt, und bald kaum mehr 40nm-Wafer bei TSMC zu ordern braucht.

In der Folge bekommt TSMC immer weniger für seine 40nm-Wafer. Und wenn die Preise billig genug sind, läßt AMD seine Ontarios zu Dumping-Preisen bei TSMC fertigen als auch seine Lowend-GPUs.

So oder so macht das Sinn, so ein Design zu haben.

Bekäme GF auch nix gebacken, braucht AMD weiter GPUs in 40nm bei TSMC und dann wohl auch erst mal erste Ontarios von TSMC, weil ja bei GF dann nix ginge.

Klappts aber bei GF, dann:

Wird AMD GPUs aus der GF-Produktion liefern, die Nvidia alt aussehen lassen. AMD wird möglichst viele GPUs bei GF fertigen, so dass Nvidia bald seinen 40nm-Kruscht nimmer los bekommt, und bald kaum mehr 40nm-Wafer bei TSMC zu ordern braucht.

In der Folge bekommt TSMC immer weniger für seine 40nm-Wafer. Und wenn die Preise billig genug sind, läßt AMD seine Ontarios zu Dumping-Preisen bei TSMC fertigen als auch seine Lowend-GPUs.

So oder so macht das Sinn, so ein Design zu haben.

SPawner

Fleet Captain Special

- Mitglied seit

- 25.08.2008

- Beiträge

- 292

- Renomée

- 4

Wenn TSMCs Prozess "world-class" wäre, ...

Leute, von Huangs Ausagen passt einfach nix, gar nix wirklich zusammen

Wer hat denn einen besseren 40nm Prozess mit ausreichender Kapazität? Ohne Alternativen ist auch die schlechteste 40nm Fertigung Spitzenklasse.

Bobo_Oberon

Grand Admiral Special

- Mitglied seit

- 18.01.2007

- Beiträge

- 5.045

- Renomée

- 190

Noch gibt es UMC, (IBM) und auch Samsung will sein Foundry-Geschäft pushen. Der Apple A4 stammt aus den Samsung-Fabs.Wer hat denn einen besseren 40nm Prozess mit ausreichender Kapazität? Ohne Alternativen ist auch die schlechteste 40nm Fertigung Spitzenklasse.

MFG Bobo(2010)

Duplex

Admiral Special

früher hat Nvidia den G92 Chip parallel bei 2 Firmen fertigen lassen, TSMC & UMC

heute fertigt Nvidia den Fermi bei TSMC only, naja der alte G92 war nicht so komplex wie heute der Fermi...

heute fertigt Nvidia den Fermi bei TSMC only, naja der alte G92 war nicht so komplex wie heute der Fermi...

Markus Everson

Grand Admiral Special

Es gäbe noch eine andere Interpretationsmöglichkeit für die "mehrere tausend Fermis" [...]

Aber wäre "we are sampling" nicht lediglich die Vorstufe zur Auslieferung? Er hat ja ausdrücklich gesagt das hunderttausende Fermis ausgeliefert _wurden_. Vergangenheitsform.

.

EDIT :

.

aylano schrieb:[...] Einerseits die Kapazität mit GF.

Dazu vielleicht wie üblich sehr früher Einführung, wo dann AMD mit 28nm wieder länger einen deutlichen Vorsprung hat.

Wieder?

.

EDIT :

.

http://www.digitimes.com/news/a20100113PD201.html

Foundry chipmakers, including Taiwan Semiconductor Manufacturing Company (TSMC), have been struggling to increase their yields on 40nm to over 70%, according to industry sources.

Zuletzt bearbeitet:

Quelle: Forum SemiAccurate: John Fruehe zur Aussprache von LlanoJohn Fruehe schrieb:All of the parts are named after texas rivers. It is written LLANO and pronounced "Lano" like "Land". In spanish it would be pronounced "yano," like "yonder".

Es wird entgegen aller bisherigen Behauptungen also "länno" ausgesprochen, nicht "yano". Wusste ich bis dahin auch nicht. Hat in diesem Thread aber eigentlich nichts zu suchen.

Zuletzt bearbeitet:

[MTB]JackTheRipper

Grand Admiral Special

- Mitglied seit

- 11.11.2001

- Beiträge

- 7.814

- Renomée

- 49

- Standort

- Reutlingen

- Mitglied der Planet 3DNow! Kavallerie!

- Aktuelle Projekte

- Folding@Home, QMC, Spinhenge, Simap, Poem

- Lieblingsprojekt

- Folding@Home

- Meine Systeme

- 2x X2 3800+

- BOINC-Statistiken

- Folding@Home-Statistiken

- Mein Laptop

- HP NC2400

- Details zu meinem Desktop

- Display

- Samsung SyncMaster 305T

- Gehäuse

- Antec P180B

Gut zu wissen, dann hatte ich es bisher auch immer falsch (spanisch) gesprochen

So wie beim RV870 vs. GT200b.Wieder?

mibo

Grand Admiral Special

- Mitglied seit

- 05.01.2003

- Beiträge

- 2.297

- Renomée

- 65

- Standort

- Hannover

- Mein Laptop

- Lenovo T450s

- Details zu meinem Desktop

- Prozessor

- Ryzen 5800X3D

- Mainboard

- ASUS B550M-PLUS

- Kühlung

- Noctua NH-U12P

- Speicher

- 2x16GB DDR4 ECC

- Grafikprozessor

- AMD 6700XT

- Display

- HP X27i

- SSD

- Samsung 860EVO, 960EVO, WD 850X

- Optisches Laufwerk

- DVD-Brenner :-)

- Netzteil

- BQ Dark Power 12 750W

- Betriebssystem

- Suse Tumbleweed / Win10 64Bit

- Webbrowser

- Firefox

1. Wegen der Die-Größe bekommen sie ca. 100 Chips auf einen Wafer. Bei 400000 Chips und 100% yield wären das also 4000 Wafer (bei 50% yield -> 8000 Wafer, bei 20% yield -> 20000 Wafer).

2. Das aktuelle A3-Stepping wird seit wann gefertigt? "SemiAccurate has heard that the A3 silicon hot lots that came back just before Christmas..." Weil das chinesische Neujahrsfest dann Anfang 2010 war (soweit ich weiß, machen da in Taiwan alle Urlaub), rechne ich also mit nem A3-Stepping-Produktionsstart am 1.1.2010.

Das "Q1 of fiscal year 2011" ging anscheinend bis zum 2.Mai ( http://seekingalpha.com/article/205...5119_sa&title=in-depth-analysis-of-nvidias-q1 ).

3. Die 400000 Chips müssen also im Zeitraum 1.1.2010 bis 2.5.2010 entstanden und ausgeliefert worden sein. Das wären also 4 Monate Zeit -> 1000 Waver/Monat (100% yield), 2000 Waver/Monat (50% yield), bzw. 5000 Waver/Monat (20% yield).

Wie realistisch sind meine Überlegungen? Wieviele Waverstarts gibts bei TSMC pro Monat überhaupt?

Edit: Upps, ich sehe gerade - das war schon auf der letzen Seite hier ein Thema gewesen

Alzheimer

http://www.xbitlabs.com/news/other/...to_Double_40nm_Output_by_End_of_the_Year.html

TSMC hat also 80000 40nm Waverstarts pro Quartal -> ca. 27000/Monat

Also wären selbst bei 20% yield die 5000 Waver/Monat theoretisch möglich. Oder weiß man, auf wieviele Kunden die 40nm Waver aufgeteilt werden?

2. Das aktuelle A3-Stepping wird seit wann gefertigt? "SemiAccurate has heard that the A3 silicon hot lots that came back just before Christmas..." Weil das chinesische Neujahrsfest dann Anfang 2010 war (soweit ich weiß, machen da in Taiwan alle Urlaub), rechne ich also mit nem A3-Stepping-Produktionsstart am 1.1.2010.

Das "Q1 of fiscal year 2011" ging anscheinend bis zum 2.Mai ( http://seekingalpha.com/article/205...5119_sa&title=in-depth-analysis-of-nvidias-q1 ).

3. Die 400000 Chips müssen also im Zeitraum 1.1.2010 bis 2.5.2010 entstanden und ausgeliefert worden sein. Das wären also 4 Monate Zeit -> 1000 Waver/Monat (100% yield), 2000 Waver/Monat (50% yield), bzw. 5000 Waver/Monat (20% yield).

Wie realistisch sind meine Überlegungen? Wieviele Waverstarts gibts bei TSMC pro Monat überhaupt?

Edit: Upps, ich sehe gerade - das war schon auf der letzen Seite hier ein Thema gewesen

Alzheimer

http://www.xbitlabs.com/news/other/...to_Double_40nm_Output_by_End_of_the_Year.html

TSMC hat also 80000 40nm Waverstarts pro Quartal -> ca. 27000/Monat

Also wären selbst bei 20% yield die 5000 Waver/Monat theoretisch möglich. Oder weiß man, auf wieviele Kunden die 40nm Waver aufgeteilt werden?

Zuletzt bearbeitet:

Ähnliche Themen

- Antworten

- 296

- Aufrufe

- 38K

- Antworten

- 264

- Aufrufe

- 69K

- Antworten

- 123

- Aufrufe

- 19K

G

- Antworten

- 1K

- Aufrufe

- 167K